Building a hydroelectric power plant is one of the most challenging endeavors globally. It requires substantial capital, years of construction, extensive regulatory approvals, and the patience to wait nearly a decade before the first unit begins generating electricity. Investors often find themselves watching debt accumulate and projects miss deadlines, with little interim progress to show.

This has been the narrative for NHPC (formerly known as the National Hydroelectric Power Corporation) for much of the past decade.

As India’s largest hydropower producer, NHPC has invested tens of thousands of crores into dams throughout the Himalayas, even as earnings growth has remained modest and returns on capital have faced pressure. The market has largely perceived it as a company that is perpetually in the construction phase without reaping the benefits of its investments.

However, this perception may be shifting. Over the past year, several long-delayed projects have begun generating electricity, with more scheduled to be commissioned in the next two years, and a significant construction pipeline is steadily nearing completion.

The question for investors is no longer whether NHPC can construct dams but whether the company is finally entering a phase where years of investment will translate into stronger earnings and cash flows.

A Utility in Transition

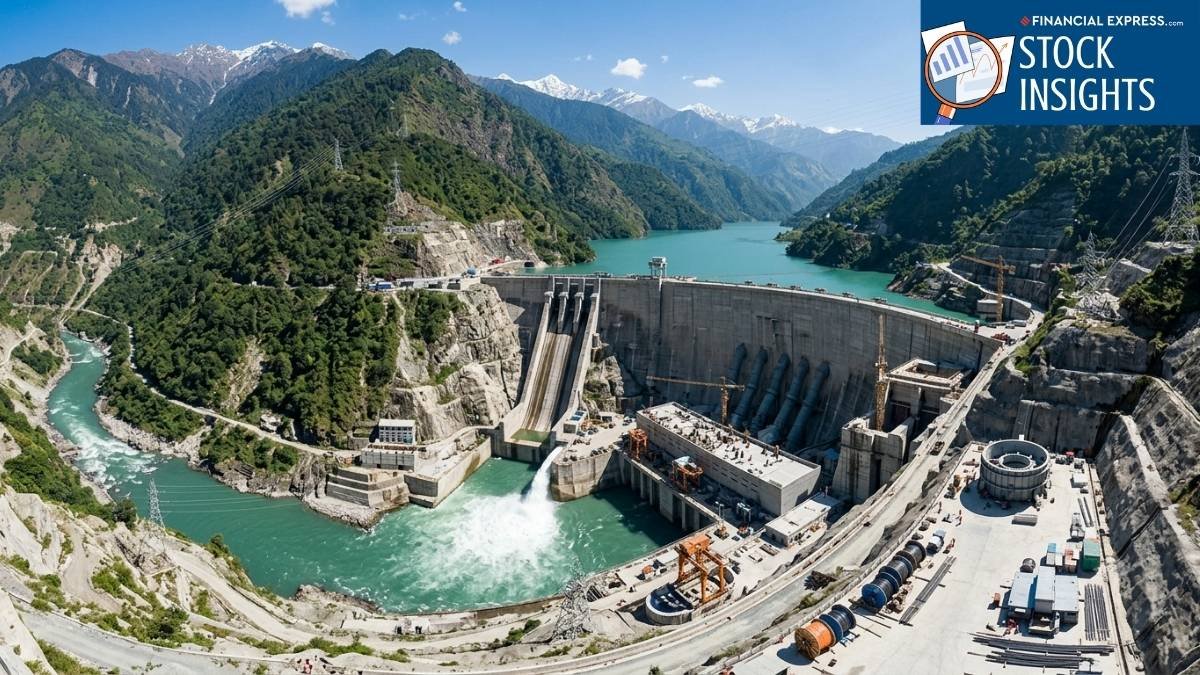

NHPC Limited is India’s largest hydropower enterprise and a Government-owned Navratna public sector company. While hydroelectric power remains its primary focus, the company has gradually diversified into solar and wind energy. It is also exploring pumped storage projects that could play a crucial role in balancing renewable energy generation.

Unlike thermal power companies that can build plants within a few years, hydroelectric projects typically take much longer due to challenging terrain, environmental approvals, geological issues, and rehabilitation requirements. Consequently, capital remains tied up for years before a project begins earning regulated returns.

This has been the case for NHPC. The company has continued to invest in large projects, but investors have seen little improvement in profitability as many of these assets were still under construction.

FY26: A Potential Turning Point

FY26 marks the first year in which multiple large projects began contributing to operations.

Revenue from operations rose by 12% to Rs 11,615 crore from Rs 10,380 crore in FY25. Additionally, consolidated power generation increased by 16% to 29,619 million units. Management attributed this improvement primarily to the commissioning of the 800 megawatt Parbati-II project, the phased commissioning of the 2,000 megawatt Subansiri Lower project, increased generation from Parbati-III and Uri-I, and contributions from the Karnisar solar project.

The rise in generation also contributed to a profit after tax increase to Rs 3,766 crore from Rs 3,007 crore during the year, according to management. However, several costs that were previously hidden while projects were under construction began to appear in the income statement. Interest expenses rose as newly commissioned assets ceased capitalizing borrowing costs and began charging them to the profit and loss account. Depreciation also increased as new assets entered commercial operations.

This partly explains why margins have not expanded in line with revenue growth. The operating profit margin was approximately 45% in FY26 compared to over 52% the previous year.

For a capital-intensive utility, this transition is not uncommon. The initial years after commissioning typically incur higher depreciation and finance costs before assets begin generating stable regulated returns.

The Future Outlook

The larger opportunity for NHPC lies not in what has already been commissioned but in the projects expected to come online in the coming years.

The Subansiri Lower project remains the most significant near-term trigger. Four of its eight units have already been commissioned, with the remaining four expected to become operational sequentially by March FY27. Once fully commissioned, it will become one of India’s largest hydroelectric power stations. The anticipated project cost is around Rs 30,072 crore, of which more than Rs 26,000 crore had already been spent by March 2026.

Beyond Subansiri, NHPC anticipates commissioning Rangit-IV by November 2026, while Kiru and Pakal Dul are targeted for FY27. Ratle is scheduled for commissioning in 2028, and Teesta-VI in 2029. The company has also commenced work on Uri-I Stage II and Dulhasti Stage II after receiving investment approvals earlier this year.

These projects represent a visible pipeline of assets that NHPC has not experienced for several years, steadily transitioning from construction to operation.

Diversifying Beyond Hydropower

While hydroelectricity will remain NHPC’s core business, the company is also expanding its renewable energy portfolio.

Under the Central Public Sector Undertaking Scheme, NHPC has already commissioned a 300-megawatt solar project in Bikaner, Rajasthan. An additional 100 megawatts in Andhra Pradesh and 600 megawatts in Gujarat are expected to be commissioned during 2026. Floating solar projects in Kerala and further developments at Khavda in Gujarat are also progressing.

Management has also highlighted another opportunity that could gain importance over the next decade. NHPC currently has around 18 gigawatts of pumped storage projects at various planning stages across Maharashtra, Odisha, Madhya Pradesh, Gujarat, Chhattisgarh, Rajasthan, and Andhra Pradesh. The company expects to begin construction of the 640 megawatt Indira Sagar-Omkareshwar pumped storage project during FY27.

Pumped storage projects are gaining attention as they help store surplus renewable electricity generated during the day and release it during peak demand. As India’s solar capacity rapidly expands, this segment could emerge as a significant growth area for utilities experienced in large hydro projects.

Financial Overview

Years of investing in large infrastructure projects have naturally increased NHPC’s borrowings.

The company has a debt-to-equity ratio of approximately 1.26 times. While leverage remains high, it reflects investments in assets that are only now beginning to contribute to earnings. Interest coverage remains comfortable at around 3.7 times, indicating that current operating profits are sufficient to cover finance costs.

NHPC’s balance sheet should be evaluated alongside the company’s construction cycle. If the planned commissioning schedule is broadly met over the next few years, a larger portion of invested capital will begin earning regulated returns instead of remaining tied up in projects under construction.

Returns on Investment

Despite operating one of India’s largest clean energy portfolios, NHPC has not been recognized for high returns on capital.

Return on Equity is around 9.3%, while Return on Capital Employed is approximately 5.7%. These figures remain below those of several listed utilities, largely because a significant portion of the capital employed has been locked in projects that have yet to become operational.

This situation could gradually improve as commissioned assets begin contributing for a full year, and more projects transition into commercial operation. Unlike businesses that require continuous expansion to maintain earnings, regulated hydroelectric assets generally provide predictable returns once operational.

Valuation Insights

At the current market price, NHPC trades at around 21 times earnings and about 1.9 times book value. The stock also offers a dividend yield of approximately 2.3%, making it relatively appealing for investors seeking a combination of regular income and exposure to India’s expanding clean energy infrastructure.